Today, bank clients expect a seamless, convenient, and personalized experience. By adopting digital transformation, banks can meet their customers' growing needs, increase operational effectiveness, and gain a competitive advantage. Moreover, digital banking transformation allows leveraging emerging technologies, data analytics, and automation to enhance decision-making, identify new business opportunities, and create innovative service offerings.

Digital transformation of banks refers to the comprehensive integration of computer technologies into all operations, fundamentally changing how financial institutions operate, interact with customers, and deliver services. It involves strategically adopting technologies to streamline processes and drive innovation in the banking industry.

This article explores the challenges and opportunities of digital transformation for banking, the technologies revolutionizing the financial sector. We will analyze the impact of digitalization on banks and customers, regulatory challenges, success stories, and the future of this transformative journey. Using the expertise of Inoxoft in banking software development services, we demonstrate how winning digital solutions, such as a Trading Automation Platform and Integrating Online Payment Services with CBS, alter the banking sector.

- Challenges and Opportunities of Digital Transformation for Banks

- Challenges of implementing digital transformation in the banking industry

- Opportunities presented by digital transformation for banks

- Technologies Driving Digital Transformation in Banks

- Artificial intelligence and machine learning

- Cloud computing

- Blockchain

- Internet of Things

- Robotic Process Automation

- Impact of Digital Transformation on Banks and Customers

- Improved customer experience

- Increased efficiency and cost savings

- New business models

- Regulatory Challenges and Risks

- Evolving regulatory standards

- Data privacy and security risks

- Technological risks

- Change management and employee skill gap

- Digital Transformation in Banking: Success Stories

- Bank of America

- ING Group

- JPMorgan Chase

- Future of Digital Transformation of Banks

- Enhanced customer experience through AI technologies

- Open banking and collaboration

- The rise of biometric authentication

- Expanded use of blockchain

- Emphasis on data privacy

- Operating like tech companies

- Consider Inoxoft Your Trusted Partner

- Trading Automatization Platform

- Integrating Online Payment Services with CBS

Challenges and Opportunities of Digital Transformation for Banks

Digital transformation entails both challenges and opportunities for the banking industry. This section explores some key challenges and opportunities banks experience during their digital transformation journey.

Challenges of implementing digital transformation in the banking industry

Legacy systems and complex IT infrastructure

Conventional banks struggle to integrate digital technologies into their legacy systems and complex IT infrastructure. These systems can be outdated, fragmented, and not designed to support innovative digital solutions. Overcoming this challenge requires careful planning, modernization of systems, and integration strategies that ensure compatibility and scalability.

Data silos and integration

Since conventional banks usually have several data sources and silos, getting a complete picture of consumer data can be difficult. A data silo is a collection of data maintained by one group within an organization that is not readily available to other groups or departments in the same organization.

Integrating data from disparate sources and ensuring data consistency and accuracy can be a significant challenge. Effective data management and integration strategies are essential for leveraging the full potential of banks digital transformation.

Data security and privacy

Consumer privacy and data security become increasingly important as banks employ digital technologies. Protecting sensitive financial information, preventing data breaches, and complying with data protection regulations present ongoing challenges. Banks must implement robust cybersecurity measures, adopt encryption techniques, and maintain compliance with regulatory standards to build customer trust.

Regulatory compliance

The banking industry is heavily regulated, and digital transformation adds another layer of complexity to regulatory compliance. Banks must navigate regulations related to data protection, anti-money laundering (AML), know-your-customer (KYC), and consumer protection. Ensuring compliance while delivering innovative digital services requires a thorough understanding of regulatory requirements and proactive compliance measures.

Opportunities presented by digital transformation for banks

Enhanced customer engagement

Bank digital transformation allows them to engage customers in new and meaningful ways. Banks can build stronger customer relationships through personalized experiences, self-service options, and omnichannel interactions. Banks can leverage data analytics, AI, and ML to offer tailored recommendations, targeted promotions, and proactive customer support, increasing customer satisfaction and loyalty.

Operational efficiency

Digital bank transformation streamlines operations, automates manual processes, and reduces operational costs. By eliminating paperwork, reducing manual errors, and improving process efficiency, banks optimize resource allocation, reduce operational expenses, and improve profitability. Automation, digital workflows, and data-driven decision-making contribute to operational efficiency.

New revenue streams

Digital transformation in banking opens doors to new revenue streams for financial institutions. Banks can expand their product offerings and tap into new market segments by collaborating with fintech startups, leveraging open banking APIs, and offering platform-based services. Additionally, innovative partnerships and collaborations enable banks to monetize their data, explore new service models, and create additional revenue streams beyond traditional banking products.

Improved risk management

Digital banking transformation allows financial institutions to enhance risk management practices. Banks can detect and mitigate fraud more effectively by leveraging advanced analytics, AI, and ML, accurately assessing credit risk, and identifying real-time anomalies. It enables proactive risk management, strengthens compliance with regulatory requirements, and reduces financial and reputational risks.

Overcoming the challenges through strategic planning, technology adoption, and organizational efficiency will help banks maximize the opportunities digital transformation presents.

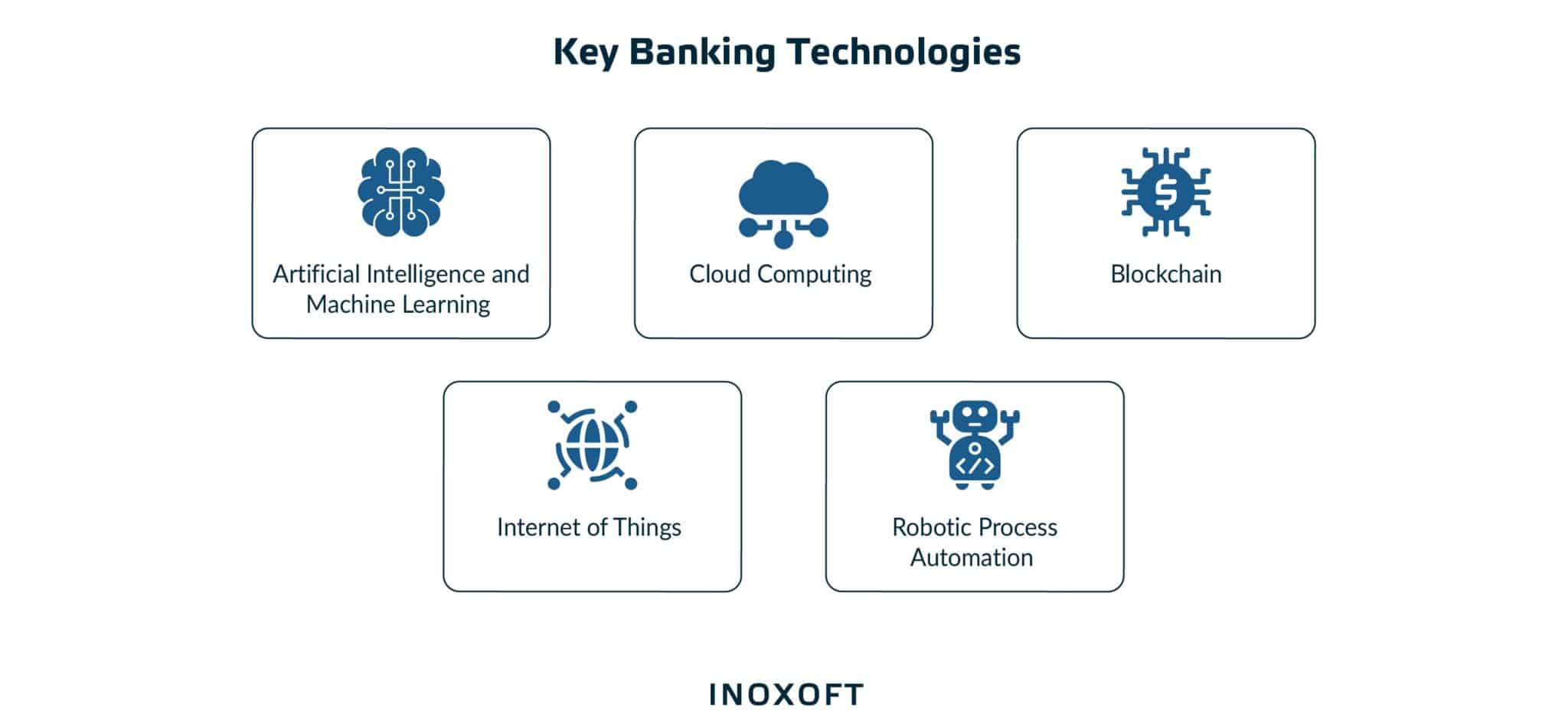

Technologies Driving Digital Transformation in Banks

Technological advancements revolutionize the banking industry, and several key technologies are driving banks’ digital transformation, enabling them to enhance customer experiences, streamline operations, and embrace innovative solutions. Let’s look closer at some of them.

Artificial intelligence and machine learning

Artificial Intelligence (AI) and Machine Learning (ML) technologies revolutionize the banking industry. AI-powered chatbots provide real-time customer support, while ML algorithms analyze vast amounts of data to detect fraud, assess creditworthiness, and deliver personalized recommendations.

Artificial intelligence is also used to manage, analyze and protect data, and provide better consumer experience. For instance, AI quickly evaluates customer data, spotting repeating trends. With machine learning, it is easier to identify changes in user behavior and take prompt preventive action.

Cloud computing

Cloud computing is one of the most common technologies banks and the financial sector use. It enables banks to securely store and process large volumes of data, providing scalability and flexibility. Improved operations, increased productivity, and immediate product and service delivery are all benefits of cloud-driven services. Cloud computing also facilitates remote access to banking services, enhances collaboration, and accelerates deploying new applications and services.

Blockchain

Blockchain adoption in the financial industry has led to safer data transfers, more precision, and improved user interfaces. This technology helps to enhance the simplicity and transparency of banking transactions. Blockchain offers robust security and efficiency in banking operations. It enables secure and traceable transactions, simplifies cross-border payments, and streamlines complex processes such as Know Your Customer (KYC) verification and trade finance.

Internet of Things

The Internet of Things (IoT) allows banks to connect devices and gather real-time data, enabling personalized experiences and efficient monitoring of assets. IoT applications in banking include smart ATMs, wearables for contactless payments, and connected devices for fraud detection. With IoT and its smart device connectivity, customers can quickly and easily make contactless payments. Risk management, authorization procedures, and access to numerous platforms introduced by IoT have entirely changed the financial environment.

Robotic Process Automation

Robotic Process Automation (RPA) automates repetitive and rule-based tasks, allowing employees to concentrate on higher-value activities. RPA improves operational efficiency, reduces errors, and enhances the speed and accuracy of back-office processes. It is used in customer support to address customer complaints, follow compliance regulations, and prevent fraud. Employing RPA allows banks to lower error rates and save costs.

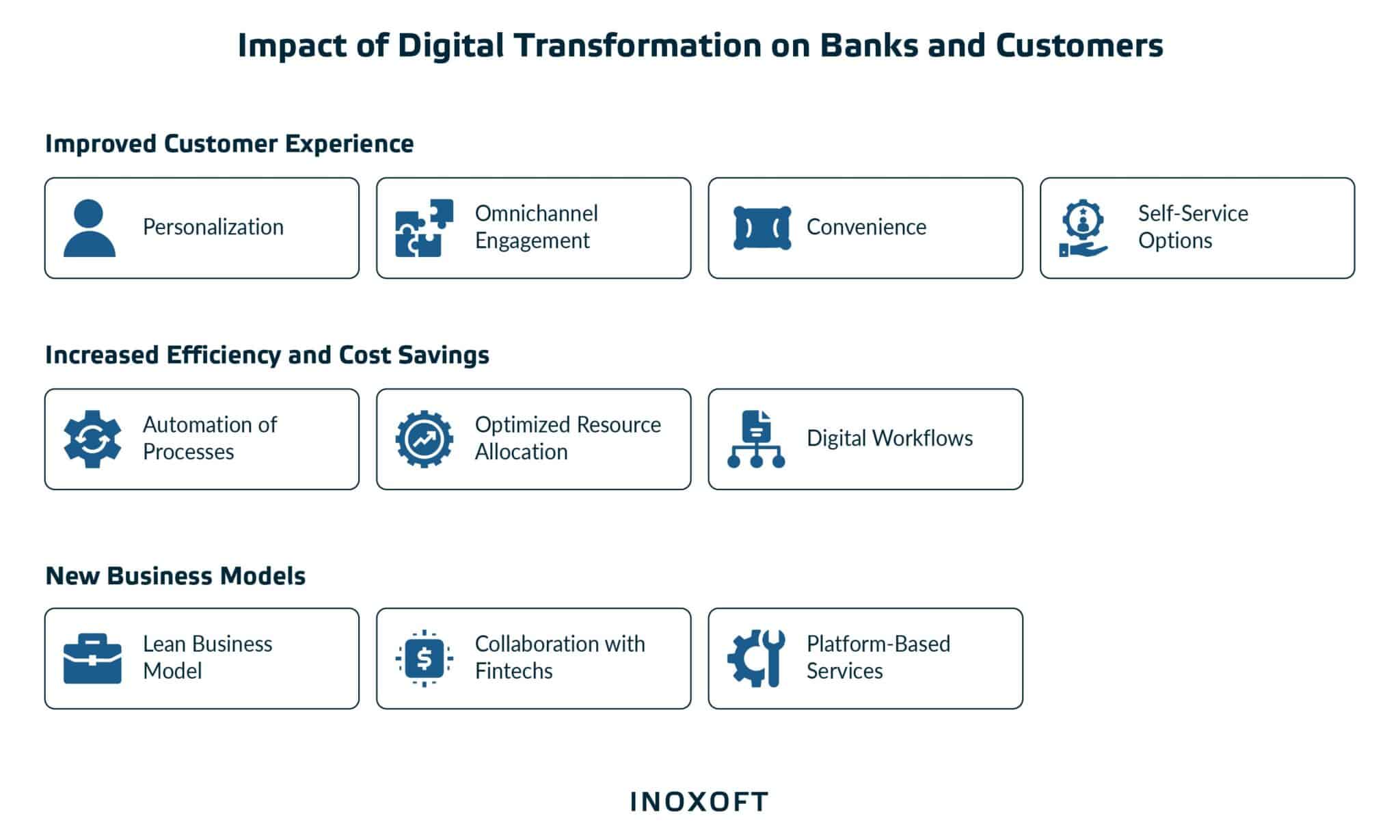

Impact of Digital Transformation on Banks and Customers

Digital transformation positively impacts the banking industry, benefiting both banks and their customers. Let’s explore some of the critical advantages that digital transformation offers.

Improved customer experience

Digital transformation enhances the customer experience by providing benefits such as:

- Personalization. Digital transformation enables banks to gather and analyze customer data, offering personalized services and recommendations tailored to individual needs and preferences.

- Omnichannel engagement. Customers can interact with their bank through multiple channels, including mobile apps, online platforms, and chatbots, ensuring seamless and consistent experiences across touchpoints.

- Convenience. Customers can access banking services anytime and anywhere, making transactions, managing accounts, and seeking support more convenient and accessible.

- Self-Service Options. Digital transformation empowers customers with self-service capabilities, enabling them to perform various banking tasks independently without needing branch visits or manual assistance.

Increased efficiency and cost savings

Digital transformation drives operational efficiency and cost savings for banks, leading to:

- Automation of processes. Digitalization allows automating manual and repetitive tasks, reducing the reliance on manual intervention and streamlining operations, which improves efficiency and reduces errors.

- Optimized resource allocation. Banks can allocate resources more effectively, optimizing workforce productivity and minimizing operational costs.

- Digital workflows. Banks improve efficiency, reduce administrative burdens, and speed up internal processes by digitizing workflows and eliminating paper-based processes.

New business models

Digital transformation opens up new avenues for banks to explore innovative business models, including:

- Lean business model. Bank efficiency is the aim of digital transformation. Putting efficiency first in employing emerging technologies, banks make their organization leaner and more competitive against neobanks.

- Collaboration with fintechs. Banks can collaborate with fintech startups and leverage their technology and expertise to offer innovative products and services to customers, expanding their market reach.

- Platform-based services. Digital transformation allows banks to transform into platform-based businesses, providing financial services beyond traditional banking offerings, such as integrating third-party services and creating ecosystems.

Digital transformation in banking contributes to improved customer satisfaction, increased operational efficiency, and innovation. As a result, banks position themselves as modern, customer-centric institutions and remain competitive in the rapidly evolving financial sector.

Regulatory Challenges and Risks

Digital transformation brings regulatory challenges and risks that banks have to address. Let’s explore the key regulatory challenges and risks associated with digital transformation.

Evolving regulatory standards

Banks need to ensure that their digital transformation initiatives comply with regulatory standards, such as Know Your Customer (KYC), Anti-Money Laundering (AML), data privacy laws, and cybersecurity regulations. Banks operating in various countries also face the challenge of complying with regulations that vary significantly from country to country. Managing compliance across borders requires a thorough understanding and adaptation to various regulatory environments.

Data privacy and security risks

Providing digital banking services, banks have to ensure the privacy and security of sensitive customer information. They must implement robust security measures, encryption protocols, and access controls to safeguard customer data and prevent breaches. As digital transformation introduces new channels and technologies, banks face cyber threats, including hacking, malware, phishing attacks, and ransomware. Investing in threat detection and prevention systems is essential to protect customer data and the bank’s reputation.

Technological risks

Implementing new technologies and systems during digital transformation can lead to operational disruptions and system failures if not properly managed. Banks must ensure robust testing and backup systems to minimize the risk of service disruptions and maintain business continuity. Integrating various digital systems, legacy infrastructure, and third-party solutions can be complex. Banks need to plan and execute integration strategies carefully to mitigate compatibility issues, data inconsistencies, and interoperability challenges.

Change management and employee skill gap

Digital transformation often requires significant organizational culture, processes, and role changes. Banks need to manage their resistance to change and ensure employee readiness to embrace new technologies and working methods. Adopting new technologies and digital tools requires banks to upskill or reskill their workforce.

Navigating these regulatory challenges and risks requires proactive measures, such as regular audits, robust security protocols, compliance training, and strategic partnerships with technology and cybersecurity experts.

Digital Transformation in Banking: Success Stories

Many banks already employ digital transformation to deliver exceptional customer experience, improve efficiency, and drive growth. Let’s explore some notable success stories.

Bank of America

Bank of America invested heavily in technology infrastructure and introduced innovative digital solutions. One of their notable successes is launching the Bank of America mobile app. The app offers a range of features, including mobile check deposits, person-to-person payments, and personalized financial guidance. Bank of America achieved significant customer adoption, increased engagement, and improved operational efficiency through its digital transformation initiatives.

ING Group

ING Group ING Group is a multinational banking and financial services corporation based in the Netherlands. The bank adopted an agile approach and implemented various digital solutions, such as the ING mobile banking app and online banking platforms. These platforms provide customers with easy access to banking services, personalized financial insights, and efficient account management. ING Group’s digital transformation initiatives have improved customer satisfaction, operational efficiency, and retention.

JPMorgan Chase

JPMorgan Chase is one of the largest banks in the United States. The bank introduced the Chase mobile app, offering features like mobile payments, account alerts, and digital wallets. Additionally, the bank invested in automation and data analytics to streamline processes and gain valuable insights into customer behavior. Their digital transformation efforts have led to increased customer engagement, reduced costs, and improved efficiency in operations.

These success stories highlight the transformative power of digital technologies. Banks achieve remarkable customer satisfaction, operational efficiency, and growth results through strategic investments in technology, customer-centric approaches, and agile implementation.

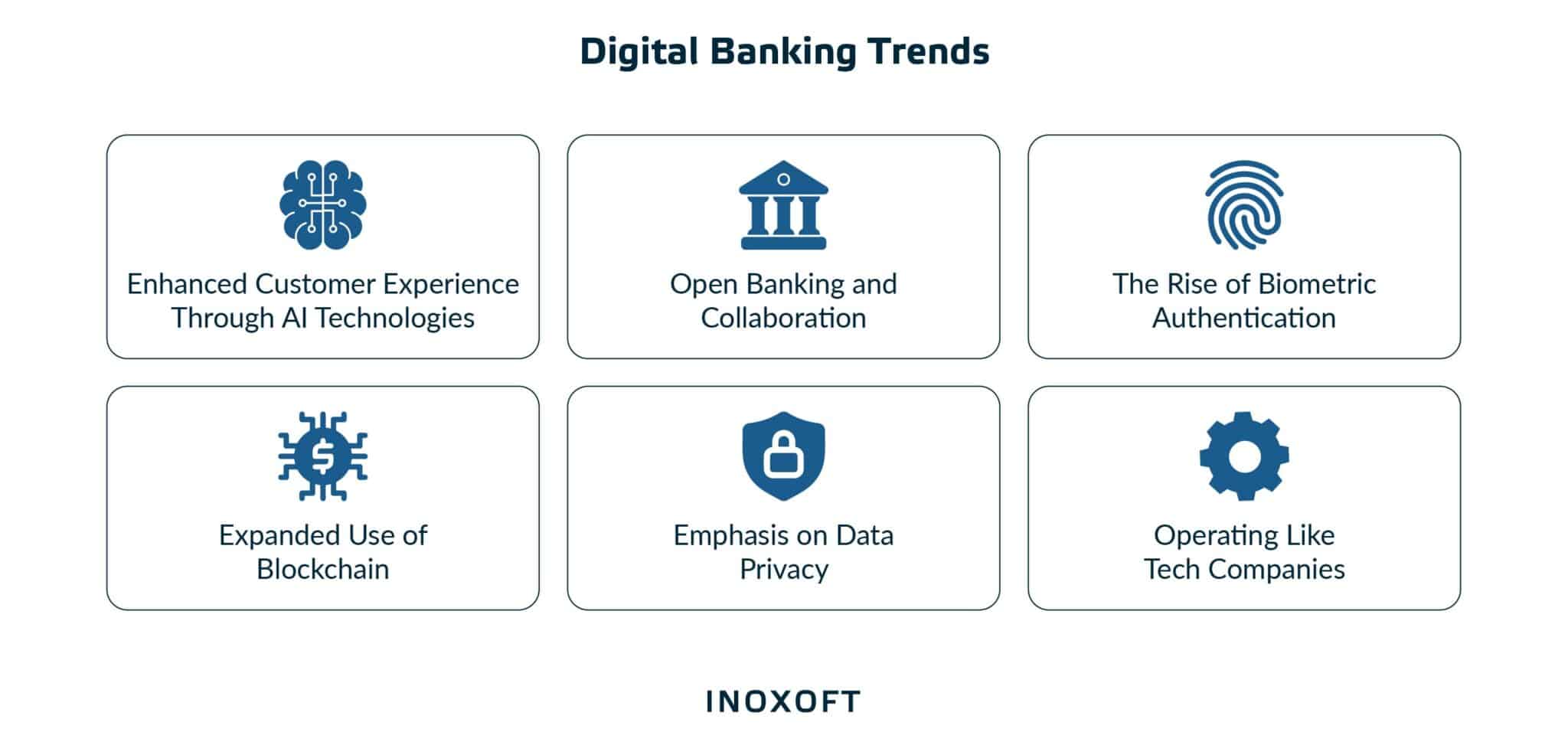

Future of Digital Transformation of Banks

Transformation is no longer a luxury but a need for banks to be competitive and relevant in today’s changing digital market. Financial organizations that don’t adopt emerging technologies risk falling behind. Let’s look at some digitalization trends that will drive the industry in the foreseeable future.

Enhanced customer experience through AI technologies

Banks will focus on delivering exceptional customer experience by leveraging AI technologies. Insider Intelligence states AI technologies can save banks around $447 billion if deployed correctly. AI-powered virtual assistants, chatbots, and personalized recommendations will become more prevalent, providing customers with tailored solutions and support.

Open banking and collaboration

The global open banking market amounted to $21.3 billion in 2022 and is expected to reach $67.8 billion by 2028, growing at a CAGR of 21.29% from 2022 to 2028. Open banking initiatives will increase collaboration between traditional and fintech companies. Open APIs will enable seamless integration of third-party services, allowing customers to access a broader range of financial products and services within their digital banking platforms.

The rise of biometric authentication

The global market for banking and financial services biometrics is expected to be worth $15.2 billion by 2030, expanding at a CAGR of 14.4% from 2023 to 2030. It implies that biometric authentication methods, such as fingerprint or facial recognition, will become more widespread, providing secure and convenient access to digital banking services. These technologies offer enhanced security and eliminate the need for passwords or PINs.

Expanded use of blockchain

The use of blockchain technology in the financial sector is anticipated to advance over the coming years, with a market value of about $22.5 billion predicted for 2026. Blockchain technology will continue to disrupt the financial industry, enabling secure and transparent transactions. Banks will explore integrating blockchain-based solutions for cross-border payments, identity verification, and smart contracts.

Emphasis on data privacy

More than 60 countries worldwide introduced a privacy or data protection regulations since the General Data Protection Regulation (GDPR) was launched in 2018. With the increasing reliance on customer data, banks will prioritize data privacy and compliance with stringent regulations. Stricter security measures, transparency, and customer consent mechanisms will be implemented to protect sensitive information.

Operating like tech companies

McKinsey claims banks will operate as tech companies to provide a market-leading value proposition. Leaders in the banking industry should act promptly to benefit from digital transformation. Data analytics, a cutting-edge technology stack, and an agile operating model are three critical capabilities banks will need to focus on proactively to stay relevant with the evolving technology.

Consider Inoxoft Your Trusted Partner

Digital transformation has revolutionized banking, providing customers with convenient, accessible, and efficient financial services. As banking services continue to evolve and embrace technological advancements, digital innovation in banking holds tremendous potential to shape the industry’s future. It transforms how individuals and businesses manage their finances.

Inoxoft is an international software development company and certified partner specializing in custom fintech software development services. We are skilled at building efficient digital banking solutions and putting creative concepts into practice with the best banking software developers in the world. Our products will boost client satisfaction, streamline processes, and guarantee security as you expand.

With Inoxoft as a trusted partner equipped with expertise in digital banking projects and a track record of solving challenges with practical solutions, you can confidently embrace the benefits of digitalization. At Inoxoft, we take security seriously and implement stringent measures to safeguard your digital banking solutions. Let’s check out our success cases.

Trading Automatization Platform

A British group of stock traders hired Inoxoft to create an app that uses algorithms to optimize data to automate tedious activities. As a company specializing in trading software development services, Inoxoft developed a web application that eliminated manual labor, produced automatic spreadsheets with data on the best exchange rates, and compiled all created orders for profitable purchases following a predetermined financial plan.

Integrating Online Payment Services with CBS

Inoxoft is a pioneer in enterprise software integration for companies of all sizes with online payment systems. To speed up the processes involved in financial transactions, we adapt “PayPal-like” online payment systems to your company’s needs. By upgrading and updating your business, we add value to it.

Contact us to discuss your bank’s digital transformation journey and get an estimate.

Frequently Asked Questions

What is digital transformation of banks?

Banks' digital transformation refers to the strategic adoption and integration of digital technologies across all banking operations, aiming to improve customer experiences, streamline processes, and drive innovation.

Why is digital transformation important for banks?

Digital transformation is crucial for banks to meet evolving customer expectations, improve operational efficiency, gain a competitive edge, and explore new business opportunities through innovative service offerings.

What technologies are driving digital transformation in banks?

Technologies such as artificial intelligence, machine learning, cloud computing, blockchain, the Internet of Things, and robotic process automation drive digital transformation in the banking industry.

What are the regulatory challenges and risks associated with digital transformation in banks?

Regulatory challenges in digital transformation include data protection and privacy regulations, compliance with anti-money laundering and Know Your Customer requirements, and managing cybersecurity risks.

What are the examples of banks that have successfully implemented digital transformation?

Bank of America, ING Group, and JP Morgan Chase are notable examples of banks that have successfully implemented digital transformation initiatives, leveraging technologies to enhance customer experiences and drive innovation.